No final de 2007, a Letónia passou por uma aguda crise financeira, que abalou o sistema bancário, provocou uma paragem brusca no fluxo de capitais (“sudden stop”), fez disparar o défice e atirou a economia para a recessão. Ao arrepio do que diziam os manuais (e até alguns oficiais do FMI, segundo consta), o Governo letão decidiu manter a sua moeda (o lat) atrelado ao euro e optou por restaurar o equilíbrio externo através de uma desvalorização interna, ao mesmo tempo que aplicava um violento programa de austeridade.

Os resultados foram impressionantes, segundo o primeiro-ministro letão, ou deprimentes, segundo Paul Krugman. Mas no meio da polémica surgiu finalmente um estudo consistente acerca da anatomia da crise e recuperação letã: Boom, Bust and Recovery: Forensics of the Latvia Crisis. O artigo, apresentado há pouco tempo no Brookings Institute, é da autoria de uma equipa de investigadores, com o celebérrimo Olivier Blanchard à cabeça. As principais conclusões são as seguintes:

1. What triggered the boom? Our answer: EU accession and belief in convergence to EU per capita incomes, cheap funds from foreign-owned banks, and optimistic expectations. The boom was healthy at the start, but, like many booms, increasingly bubbly and unbalanced at the end.

2. What ended the boom? The end came in two steps. First, starting in 2007, a slowdown, due to rising inflation and loss of competitiveness, and tightening credit reflecting increasing worries by banks about their loan book. Then, at the end of 2008, a collapse due to the world financial crisis, leading to a sudden stop, a credit crunch, a sharp drop in exports and increased uncertainty. Fiscal austerity came, for the most part, later.

3. What role did the sudden stop play in explaining the sharp decline in output? Liquidity provision by both foreign banks and by the central bank and the Treasury reduced but did not eliminate the credit crunch. The decline in output was larger however than what one would expect a credit crunch to trigger. Uncertainty, after the sudden stop, and the option value of waiting, probably contributed too.

4. What was the role of fiscal consolidation? Ironically, it is hard to blame fiscal austerity for the decrease in output. Much of the fiscal adjustment was implemented after the main fall in output. There is suggestive evidence that commitment to a clear adjustment program—backed by substantial international financial support—increased confidence, as reflected in lower CDS spreads. Much of the decrease in borrowing rates for households and firms was associated however with the increased credibility of the peg and the decrease in exchange rate risk. This may have been in part the indirect result of fiscal consolidation through market perception that consolidation would make the disbursement of international support more likely.

5. How did the internal devaluation work? It worked, but in ways different from the textbook adjustment. Public wages decreased sharply, but with limited effects on private wages. Much of the improvement in unit labor costs, especially in the tradable sector, came from increases in productivity. This improvement in unit labor costs was only partly transmitted to prices, leading more to an increase in margins for firms. This improvement was followed by an increase in exports, and in turn by an increase in internal demand. On the supply side, part of the adjustment has happened through emigration, in a way very similar to what happens across U.S. states.

6. Is output back to potential output and unemployment back to the natural rate? Not yet, but they may not be very far. There is no evidence that the natural rate is any higher than it was before the crisis. But the evidence is also that, given the market friendly labor market institutions, it was surprisingly high before the crisis. The difficulty is to pin down what exactly it was before the crisis.

Chamo a atenção para dois elementos importantes, pelas implicações que podem eventualmente ter para os países da Zona Euro.

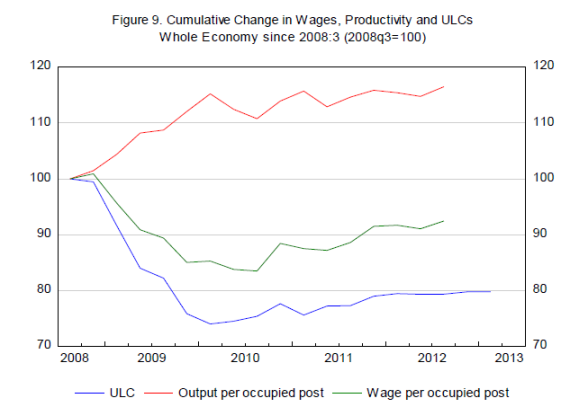

O primeiro é o funcionamento da desvalorização interna. Na Letónia, como em Portugal, houve fortes reduções dos salários nominais. Mas lá, como cá, as reduções operaram sobretudo através dos cortes administrativos do sector público. Fora desse nicho, os salários nominais revelaram uma enorme rigidez nominal à descida. A imagem de baixo mostra que os salários estavam, em 2013, quase 10% abaixo do pico atingido em 2008. Mas quando se olha apenas para o sector das manufacturas, a imagem já dá conta de um crescimento acumulado de 5%.

Note-se também que grande parte destes cortes salariais não foram passados para os preços finais, o que implicou uma redução do wage share na totalidade da economia (à semelhança do que se passa em Portugal). O determinante mais importante da redução dos custos unitários do trabalho (CUT) foi, portanto, o forte crescimento da produtividade, continuando uma tendência que já vinha de longe.

Outro ponto importante tem que ver com o impacto da consolidação orçamental. Esta é propositadamente deixada de fora da análise porque, ao que parece, surgiu depois da recessão. O pacote de austeridade só surgiu quando a economia já tinha batido no fundo, como confirmei no Eurostat (e ao contrário do que acontece com Portugal).

Segundo os autores, a recessão deveu-se, sobretudo, ao colapso da procura externa e, sobretudo, aos problemas financeiros e incerteza subsequente – questões que estão, ou estavam, umbilicalmente ligadas à capacidade do Governo letão em assegurar a paridade euro-lat. Assim que a estabilidade cambial foi assegurada, a economia voltou a crescer, recuperando rapidamente o terreno perdido e contrabalançado o choque negativo associado ao ajustamento orçamental.

Qual a relevância deste caso? É que a periferia da Zona Euro tem estado sujeita precisamente ao mesmo tipo de ‘dúvidas cambiais’ que pairaram sobre a Letónia. O que levanta uma questão importante: se as dúvidas em relação ao câmbio letão levaram, por si mesmas, a uma quebra de casa 20% do PIB, qual terá sido o impacto da reemergência do risco cambial em Portugal, Grécia, Irlanda e Espanha?

É que este risco ganhou força em meados de 2010, precisamente quando os pacotes de consolidação orçamental começaram a ser desenhados. Como os dois fenómenos caminharam lado a lado, qualquer análise dos efeitos nefastos de um está (quase) necessariamente contaminada pelos efeitos do outro. Na prática, seria impossível perceber se a recessão era produzida pela consolidação orçamental, ou pela fragmentação financeira na união monetária.

Ou seja: será que, uma vez removido o risco cambial – como tem vindo a ser -, as economias periféricas poderão voltar a crescer? É curioso notar que o crescimento aparentemente voltou no segundo trimestre de 2013, precisamente numa altura em que os riscos em torno do colapso do euro parecem definitivamente afastados (embora o processo tenha sido lento: o discurso will-do-whatever-it-takes de Draghi remonta a Julho de 2012). A minha intuição é que a hipótese é demasiado rebuscada. Mas é sem dúvida importante perceber ao certo qual o papel que a fragmentação financeira teve no colapso económico da periferia. O caso da Letónia pode ajudar a lançar alguma luz sobre esta questão.

{kind=link}

{kind=link}